If you follow the financial news on a regular basis, you certainly heard about the most recent debt figure released by Statistics Canada: Household debt to disposable income hit 163.3% by the end of 2014. In plain English, it means that for every $100 of disposable income, Canadians owe $163.3 in debt.

In other words, we are trapped in a vicious debt cycle.

After years of observing people struggle with their debt load, I was able to clearly identify the myths that trap people in debt. In fact, I was able to identify at least 8 of them!

In this post, I will reveal 4 ; and in my next blog post, I will discuss the remaining 4.

Myth #1 – The bank approved me so I must afford it

Truth is the bank’s approval criteria have nothing to do with your actual budget. We tend to forget a basic concept when it comes to the banks: they are in the business of making money by giving out loans and mortgages. When the bank approves you for a loan/ mortgage, they have no idea how much you are currently spending on eating out, vacation, private schools or clothing.

Strategy: When the bank approves you for a certain loan amount, do not immediately sign off on it. Instead, go home, plug it into your budget and see how it REALLY affects your cash flow.

Myth #2 – I don’t need an emergency fund. That’s what my line of credit is for.

Truth is your line of credit is NOT your money. Life happens and your line of credit should not be your first backup plan. A real emergency fund is made up of your own cash savings.

Strategy: Start saving for a rainy day fund today, even with as little as $50/month. Important step is to start, and stop delaying it ‘til “someday” or “later”.

Myth #3 – I have to take advantage of the low interest rates

Truth is lending rates are at their lowest level in history, yet debt levels are at their highest level ever. This stems from the fact that we, human beings, have a fear of missing out. We believe that if we don’t take advantage of the low interest rates by borrowing, we will be left out. So we jump on the bandwagon and take it as our responsibility to revive the economy.

Strategy: Take an honest look at the reasons you are borrowing. Is it to acquire an investment asset that appreciates over time? Or is it to cover your spending excess?

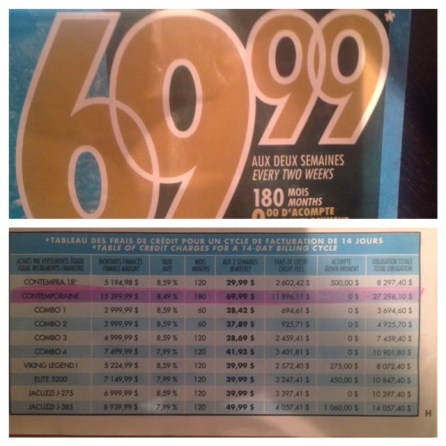

Myth #4 – It only costs $xx per month (or per 2 weeks)

Truth is our brain comprehends smaller numbers faster than large numbers. Retailers know this very well. So they show you the prices in small comprehensible amounts. However, they leave out a very important piece of information, which is the total interest cost over the lifetime of the financing.

I recently saw in a flyer, the amazing price of $69.99 for an in-ground pool! That was the price advertised using a huge font size. In a tiny illegible font all the way on the back of the flyer, it says this is the payment every 2 weeks, for a pool costing $15,400, financed at 8.49% over 15 years, for a total interest cost of $11,897. Our brain, however, focuses on the $69.99 and discards everything else.

Strategy: Ask the retailer to give you the total interest that you will be paying over the lifetime of the financing and add it to your initial cost to see how much the purchase will really be. (In the case of the above-mentioned pool it will be $15,400+11,897 = $27,297 vs the $69.99 advertised)

Stay tuned next month for my 2nd series of debt myths…

In the meantime, I suggest you apply these strategies so you stop falling into more debt traps.

{kind=link}

{kind=link}

{kind=link}

{kind=link}